Few questions arrive at our underwriting desk more often than this one. Does a surety bond protect me? The question is reasonable. The instrument is called a “bond.” It is sold by insurance companies, it is paid for with a premium, and it is frequently bundled in advertising next to general liability and workers’ compensation. It looks, sounds, and is shelved like insurance. It is not. Understanding the answer to “Does a surety bond protect me?” is the difference between confidently growing a business and being blindsided when a claim lands.

My blog piece here gives you the candid, scholarly answer the marketing brochures rarely deliver: a surety bond does not protect the principal who buys it. It protects somebody else entirely. But it does something equally important to (and indirectly, for) the principal, and that distinction is the heart of suretyship.

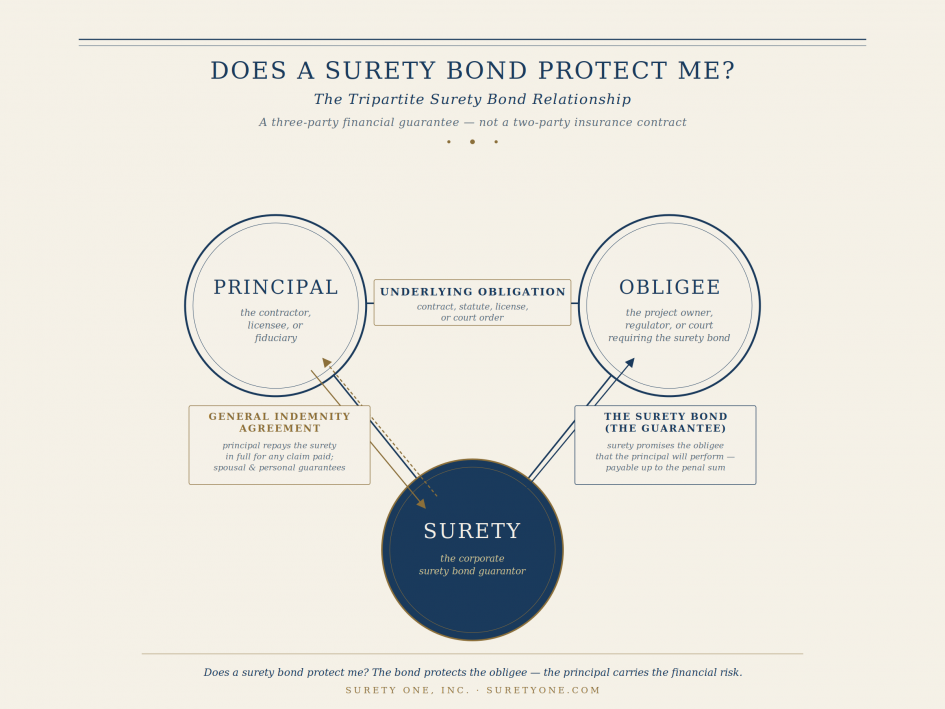

The Three-Party Architecture of a Surety Bond

A surety bond is not a two-party indemnity contract like an insurance policy. It is a tripartite financial guarantee. The U.S. Small Business Administration defines it plainly: a surety bond is a three-party instrument between a surety, who agrees to be responsible for the debt or obligation of another, a contractor, and a project owner; the agreement binds the contractor to comply with the contract’s terms and conditions (SBA 2025). The three parties are the principal (the party performing an obligation), the obligee (the party requiring and protected by the bond), and the surety (the corporate guarantor standing behind the principal’s promise).

Insurance, by contrast, is a bilateral risk-transfer mechanism. The insured pays a premium calculated on actuarial loss expectancy, and the carrier accepts risk of loss to the insured. A surety bond inverts this completely. The surety is not transferring risk away from the principal; it is lending its credit and balance sheet to the principal so that an obligee will trust the principal to perform. The premium is not priced on expected loss — it is priced on the cost of underwriting and capital deployment, because surety bonds are underwritten on a zero-loss philosophy in which the principal, at the time of execution, must appear capable of performing without loss to the surety. When a claim is paid, the principal repays the surety in full.

So when a prospect asks, “Does a surety bond protect me?” the honest, technically correct answer is: the bond is positioned to protect the obligee against your default. If it pays, you are obligated to make the surety whole.

Why a Surety Bond Does Not Protect the Principal

Three legal and structural features make this clear.

The obligee is the named beneficiary. A surety bond’s penal sum is payable to the obligee (a state licensing agency, a project owner, a federal agency, a court, or a consumer harmed by a licensed business). The principal has no right of recovery under the bond itself. As one prominent construction-law analysis observes, although courts have imposed insurance-like duties such as claims-handling procedures on sureties, bonds are not insurance policies (Gibson 2021).

The General Indemnity Agreement (GIA) makes the principal personally liable. Before any surety bond is issued, the principal (every owner with a 10% or greater interest, spouses and third-party indemnitors) signs a GIA. This contract gives the surety the contractual right to recover every dollar paid on a claim, plus loss-adjustment expense, attorneys’ fees, and investigative costs. The indemnity obligation is joint and several, generally non-negotiable, and survives the closure of the underlying project. The signature of a non-owner spouse is not a bureaucratic formality; it exists to defeat asset transfers between spouses that would otherwise frustrate the surety’s recovery.

The surety is statutorily and contractually entitled to subrogation and salvage. When the surety performs on a defaulted contract or pays a license-bond claimant, it steps into the shoes of every party it has made whole and pursues the principal’s contract proceeds, equipment, receivables, and personal assets pledged under the GIA.

Put bluntly, when somebody asks, “Does a surety bond protect me?” they should hear this in response. The surety bond is the mechanism through which a regulator or project owner is given recourse against you. The principal carries one hundred percent of the financial risk. The surety has merely accelerated the regulator’s or obligee’s ability to collect on it and loaned you its capital to back your obligations.

What a Surety Bond Actually Does for the Principal

Saying the principal is unprotected is not the same as saying the principal receives no value. A surety bond is one of the most powerful commercial enablers available to a small or mid-sized business, but the value is access, not indemnity.

It unlocks markets that would otherwise be closed. In contract suretyship, this is dispositive. The Miller Act, codified at 40 U.S.C. §§ 3131–34, requires contractors in privity with the United States to post performance and payment bonds on certain construction contracts (ConsensusDocs 2024), and every state has adopted a “Little Miller Act” applying parallel requirements to public works. Without a surety bond, federal and most public construction work is legally inaccessible. Private owners, lenders, and general contractors increasingly demand bonds for the same reasons. For a thorough scholarly treatment of how contract surety bonds function as instruments of market access, prequalification, and disciplined growth in construction, readers should consult C. Constantin Poindexter’s The Contractor’s Guide to Surety Bonds: A Primer on Contract Surety Bonding for Construction Professionals (Poindexter 2025), which traces the doctrine from common-law guaranty through modern Miller Act jurisprudence and remains the most accessible treatise on contract surety mechanics for non-attorneys.

It transmits credibility. A bonded contractor, dealer, freight broker, or fiduciary has been third-party vetted. The surety has reviewed credit, financial statements, work-in-progress, character references, and (for contract surety) construction-CPA-prepared financials. Obtaining a bond is itself a market signal. Sureties operate, in effect, as a private prequalification system that obligees rely on without paying for it.

It enables small-business participation in public contracting. The SBA’s Surety Bond Guarantee Program exists precisely because access to bonding determines access to opportunity. The program was designed to increase small-business access to federal, state, local, and private-sector contracting by guaranteeing bid, performance, payment, and specified ancillary bonds for small and emerging contractors who cannot obtain bonding through regular commercial channels (Congressional Research Service 2022). Statutory limits now reach $9 million for ordinary contracts and up to $14 million for federal contracts when justified.

It imposes useful financial discipline. Underwriting forces the principal to maintain accurate financial reporting, manage backlog, and plan for working capital — precisely the practices that prevent the defaults the bond is written against in the first place.

So the proper frame of “Does a surety bond protect me?” is this. The surety bond does not indemnify you, but it qualifies you, distinguishes you, and admits you to revenue you could not otherwise reach.

The Distinction in Commercial Versus Contract Surety

The “Does a surety bond protect me?” question carries different practical weight depending on the bond classification. In commercial surety, i.e., license and permit bonds, court bonds, fiduciary bonds, public official bonds, ERISA fidelity bonds — the bond is almost purely a regulatory or statutory compliance instrument. The obligee is usually a government body or a class of consumers, and the principal’s exposure is bounded by the penal sum and the GIA.

In contract surety, the financial stakes are larger, and the principal’s potential indemnity exposure can exceed the penal sum because the surety’s losses include completion costs, consultants, and litigation. For contractors specifically, Poindexter (2025) is the recommended primer on how the Miller Act, Little Miller Acts, GIA mechanics, and bond-account prequalification interact across the lifecycle of a bonded project.

My Parting Thoughts

Returning to the headline question, does a surety bond protect me? No. The bond is not a shield around the principal. It is a guarantee, financed by the principal, that a third party will be made whole if the principal fails. It is correctly understood as a credit product, not an insurance product. The principal repays every dollar.

But a surety bond is also the mechanism by which licensed businesses operate, contractors win public work, fiduciaries take their appointments, freight brokers move loads, and regulators trust the marketplace. In that sense, the bond is indispensable. Not because it protects the principal, but because it allows the principal to be entrusted in the first place.

If you are evaluating whether a surety bond is right for your business, or if you have been asked for one and are uncertain about the indemnity implications, the team at Surety One, Inc. can walk you through the structure, the GIA, and the appropriate program for your circumstances.

~ C. Constantin Poindexter, MA, JD, CPCU, AFSB, ASLI, ARe, AINS, AIS, CPLP

Bibliography

- ConsensusDocs. 2024. “Miller Act Bonding: Requirements and Waiver.” ConsensusDocs.

- Congressional Research Service. 2022. SBA Surety Bond Guarantee Program. Report R42037. Washington, DC: Library of Congress.

- Gibson, C. Andrew. 2021. “Surety Bonds vs. Subcontractor Default Insurance: Considerations for Construction Projects.” Stoel Rives LLP.

- Poindexter, C. Constantin. 2025. The Contractor’s Guide to Surety Bonds: A Primer on Contract Surety Bonding for Construction Professionals. San Juan: BookBaby.

- U.S. Small Business Administration (SBA). 2025. “Surety Bonds.” U.S. Small Business Administration.

- 40 U.S.C. §§ 3131–3134 (Miller Act).